The term governance refers to a system by which an organization is run. Corporate governance is the module for fixing a liability on corporate entity. Corporate Governance is the application of best Management Practices, Compliance of Laws in true letter and spirit and adherence to ethical standards for effective management and distribution of wealth and discharge of social responsibility for sustainable development of all stakeholders.

Tag: corporate governance

The Story Behind Japan’s Corporate Governance Reforms

Frequent visitors to our blog are likely aware of Japan’s major corporate governance reforms, but not everyone is familiar with the story behind how these reforms were crafted. The eminent Steven K. Vogel (Professor of Political Science at the University of California, Berkeley), recently wrote a concise and easy-to-follow history of the major reforms to Japanese corporate governance practices since the 1990s, describing how and why they came to pass.

Public Comment to the METI Fair M&A Study Group (by Nicholas Benes)

As the person who initially proposed the Corporate Governance Code to the LDP in 2013 and 2014, I am well aware of its limitations in various areas. For this reason, I am very pleased that Fair M&A Study Group have decided that its discussions should cover not only MBOs, but also ”cases which are likewise significantly affected by the issues of conflict of interest and information asymmetry”[1], including “cases of acquisition of a controlled company by its controlling shareholder.”[2]

This indeed an important mission, because these topics include virtually all types of M&A transactions and the public statements of executives and boards with regard to them. For many years in the post-war era, the failure of the government and the JPX/TSE to set forth clear bright-line rules that facilitate a fair, robust M&A market in Japan has stunted productivity, dynamism and growth in the Japanese economy.

Amended, Detailed Public Comment by Nicholas Benes to JPX re: “Review of the TSE Cash Equity Market Structure”

NOTE: This public comment supersedes and replaces the one that I, Nicholas Benes, submitted on January 12, 2019)

As the person who initially proposed the Corporate Governance Code to the LDP in 2013 and 2014, and suggested a number of principles in it, I am well aware of its limitations in various areas and the fact that Japan has not yet attained the quality level for an equity market that is expected by global investors. In this sense I am very pleased that the JPX has decided to review its equity market structure and related standards.

Challenges and Realities

This indeed an important mission, for which is it essential to recognize and discuss the impact of a number of challenges that Japan faces in improving governance, efficiency, and trustworthiness of its equity capital markets. These challenges include:

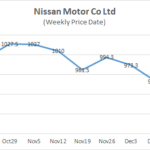

Damages Estimation- How Much Will Nissan Have to Pay to Investors?

Mr. Ghosn’s criminal cases are ongoing. But the criminal cases alone will not put a close to this entire ordeal. It is a matter of time for Nissan to face civil cases filed by investors. Due to Mr. Ghosn’s understated compensation, it is anticipated that a considerable amount of assets will flow out of Nissan. The largest part of this outflow will be accounted for the damages claimed by and awarded to investors in civil lawsuits. What amount of assets will flow out of Nissan? This memo is an attempt to estimate the probable size of these damages.

5 Myths About Digitizing the Boardroom

Recent advances in technology have sparked a seismic shift in how companies operate and communicate. At the boardroom level, paper systems are drifting out and being replaced with upgraded tools and processes that streamline board activities.

You may be struggling to pinpoint the true benefits a board portal may bring to your organization, or you may have some assumptions about the technology that is inhibiting you from looking into a solution further.

This checklist spotlights some of the most common myths about digitizing the boardroom, and will illustrate the ways board portal technology can streamline information sharing and accelerate collaboration.

RIETI Paper: “Corporate Governance, Employment, and Financial Performance of Japanese firms: A cross-country analysis”

Abstract: “This study examines whether the sustained lower profitability and market valuation of Japanese firms compared to global peer firms can be explained by the structure of insider dominate board of directors and the employment system which hinders flexible employment adjustments by using cross-country data. Firstly we show that level of outside director ratio and flexibility of employment adjustment both differ consistently across 27 countries in the analyzed period. We show that these two factors significantly explain observed variation of financial performance across countries significantly. In addition, we show that not only do these two factors have significant explanation power over the relatively poor performance of Japanese firms, but also over the better financial performance and growth rate of US firms. ”

Authors: ARIKAWA Yasuhiro (Waseda University) / INOUE Kotaro (Tokyo Institute of Technology) / SAITO Takuji (Keio University)

Download the paper: “Corporate Governance, Employment, and Financial Performance of Japanese firms: A cross-country analysis”

Related page on RIETI web site: https://www.rieti.go.jp/en/publications/summary/18120006.html

Why Corporate Governance is Central to Japan’s Growth Strategy

Just to add a few additional points in addition to Nick’s insightful comments–> Given (a) evidence that productivity in Japan is very strongly influenced by investment-specific technology, and (b) evidence that services sectors in the non-IT sector were “left behind” while manufacturing and IT sectors were able to capitalise on the technology boom, it makes sense to focus efforts on structural reform in the services sector.

Still, as Fukao, Miyagawa and Hisa demonstrated in their 2012 paper,increasing intangible capital alone has proven no indicator of rising TFP in the services sector. This may explain why policies designed to promote growth via intangible investment in services sector in the early 2000’s were misplaced.

So what are the policy alternatives? The second TFP paper gives us some key policy ingredients: