Metrical has previously published “Retirement of treasury stock and performance, corporate governance” and “Dividend policy and performance, corporate governance,” and in the articles we have examined the relationship between share retirement and performance and corporate governance, and between dividend policy and performance and corporate governance, respectively (please contact us if you would like to know more). The current article on equity issuance is the third in a trilogy. Surprisingly, interesting analysis results were confirmed for each of these approaches.

To summarize the previous two articles, the stock retirement score is positively correlated with ROA (actual) and Tobin’s q, and companies that have retired their own shares three or more times have significantly better key performance indicators in ROE (actual), ROA (actual), and Tobin’s q. Similarly, in evaluating corporate governance practices (including actions), the Metrical Corporate Governance Score, the % of Independent Directors, the Equity Issuance Score, and the Dividend Policy Score, the 100 companies that have retired their own shares three or more times have significantly higher scores than the companies that have retired their shares less frequently. This confirms that these companies have a strong awareness of the need to improve their corporate governance, as these scores are significantly higher than those of the companies that have retired their own shares less frequently.

The Dividend Policy Score has a certain relationship with the Key Performance Indicators. Companies with a payout ratio target or forecast of less than 10% have the lowest ROE (actual) and ROA (actual) as key performance indicators compared to the group with the higher dividend policy score, while they have the highest Tobin’s q. In addition, companies with a payout ratio target or forecast of less than 10% have the lowest dividend policy score compared to the group with the higher dividend policy score in the Metrical Corporate Governance Score, Equity Retirement Score and Equity Issuance Score as an evaluation of corporate governance practices (including actions). These companies have the lowest Corporate Governance Score, Equity Cancellation Score and Equity Issuance Score compared to the group with the higher Dividend Policy Score. Therefore, it can be pointed out that these companies may have relatively low awareness of improving corporate governance.

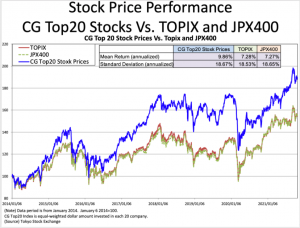

Metrical evaluates the Equity Issuance Score according to the type of equity issuance (capital increase, CB, WB, preferred stock, etc.) and the frequency of such issuance. Specifically, if a company has never issued equity since 2000, the score is 0, and if it has subsequently implemented equity financing, the score is lowered according to the type of issuance. Specifically, the score is -2 for capital increases that directly issue new shares and -1 for equity financing that mitigates the dilution of shareholder interests, such as CB, WB, and preferred shares, and a negative score is added for each equity financing.

The number of companies with an Equity Issuance Score of 0 (no equity issuance since 2000) is 797, the number of companies with an Equity Issuance Score of -1 (has issued equity only once using CBs, WBs, preferred shares, etc. that are not directly dilutive) is 121, the number of companies with an Equity Issuance Score of -2 (has raised capital once or has issued equity twice using CBs, WBs, preferred shares, etc. that are not directly dilutive) is 557, and the number of companies with an Equity Issuance Score of -3 (has issued more equity than the above) is 69, the number of companies with an equity issuance score of -4 (has issued more equity than the above) is 118, and the number of companies with an equity issuance score of -5 or lower (has issued more equity than the above) is 54.