by Nicholas Benes

This year, Japan’s governance reform drive will either keep going, or run out of steam. Judging from the amendment of the Company Law that is now underway by an advisory council of the Ministry of Justice (MOJ), the latter is likely.

Strikingly absent is a clear over-arching vision of the most important themes that amendment of the Company Law should address now that the country has a corporate governance code. In other words, what is missing, that can only be addressed via the Company Law?

If the government were truly intent on bringing about behavioral change on the part of all Japanese boards and executives, it would focus on harmonizing key aspects of the confusing array of three different corporate governance models which listed companies can adopt, and moving towards a more consistent version of the “monitoring model” for governance that has become internationally accepted and is now embodied in its own corporate governance code.

To do this, it would change the law to enable boards to flexibly appoint capable (and legally accountable) senior executives from a much wider range of candidates than is currently possible. It would also establish rules that require boards to fulfill the independent supervisory and oversight roles envisioned for them under the corporate governance code, unaffected by managerial self-interest, if they wish to delegate wider authority to executives and pay them incentive compensation determined solely by the board.

Most modern companies have a number of “executive officers” who report to the board and are accountable to it. CEOs, CFOs, and COOs are the most frequent examples, and there can be many other types. But when one says “executive officer” in Japan, one usually uses one of two words that are virtually indistinguishable in the Japanese language (shikkouyaku and shikkouyakuin; 執行役、執行役員) , but which mean very different things in terms of legal accountability

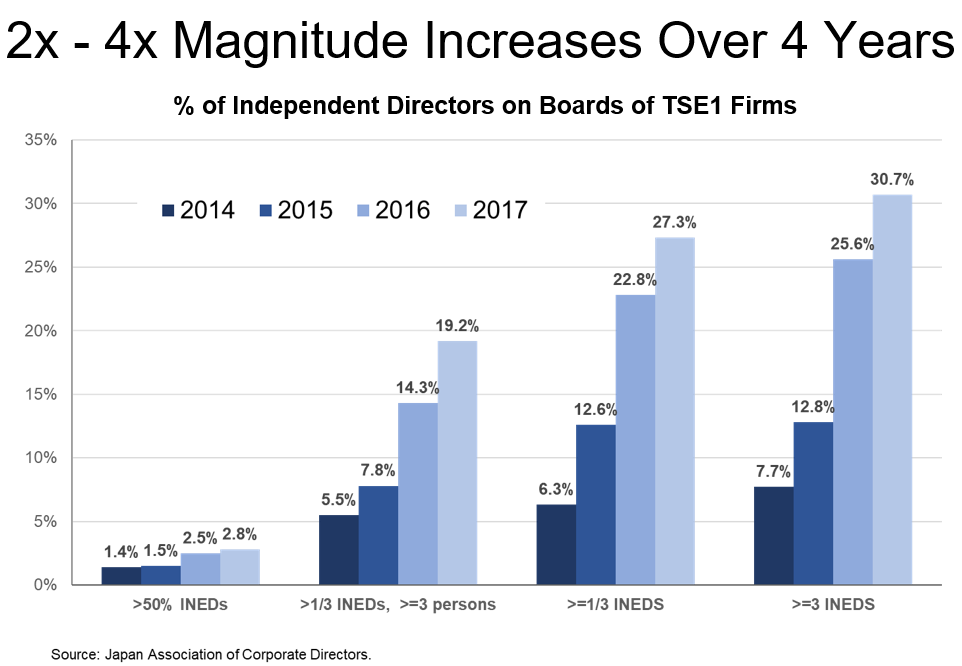

In one corporate governance model, the “the committee-style” company, shikkouyaku are legally defined executive officers under the Company Law who bear the same fiduciary duties as directors, and can be sued by shareholders for violating those duties. These “executive officers” need not be directors to be appointed as CEO, CFO, or COO. This makes good sense, because the most important aspect of “monitoring” by boards that is the selection and termination of the most suitable managers at any particular time, and there is no guarantee that such persons will already be sitting on the board when a change is needed. At the same time, the possibility of replacement from a large pool of possible candidate increases incentives for executives to perform. Unfortunately, only about 1.5% of Japanese listed companies have adopted this model of governance, which does not require a majority of independent directors on the board.

In contrast, in the two other governance models, shikkouyakin are persons who may be appointed by the board, but have no role that is defined by the Company Law, have no legal duties beyond those of normal employees, and therefore cannot be sued by shareholders. In such companies, for practical purposes shikkouyakuin make many decisions, or propose them upwards to the board for rubber-stamping. Granted, in these companies one cannot be the “representative director” (CEO) or “executive director” (業務執行取締役)at the top of the pyramid unless one has first been elected as a director by shareholders, in which case he or should could be sued by them. But conversely, this means that the very top executive positions – CEO, CFO, COO equivalents – can only be selected from a very small pool of candidates: directors already sitting on the board.

That’s not a lot of competition. In a crisis such as occurred at Olympus or Toshiba, or when a sharp change in strategy is needed, it means the board either has to select a CEO’s successor from the small number of crony directors he selected, or hurriedly stage a chaotic shareholders meeting to appoint new directors. It also means that as the number of independent directors increases (as it now is, due to the governance Code), the future pool of successor candidates will become even more narrow and less competitive. Japanese corporate governance faces both this “limited selection pool” problem, and also the accountability problem that arises in the case of the many de facto “executive officer” shikkouyakuin who do not sit on the board.

At the same time, many Japanese companies are hobbled by rules in the Company Law that require old-style “management boards” to approve all significant management decisions, because they have limited ability to delegate them to executives. This results in slow decision-making, undynamic strategies, and sluggish reallocation of assets to best uses, – all of which lead to low profitability and growth.

For these reasons, amendment of the Company Law should focus most on the following reforms:

- Defining “shikkouyakuin” under the law as an “executive officer” role that carries fiduciary duties and can be sued by shareholders, and permitting boards in approximately 98.5% of Japanese listed companies (those with the two main governance models) to appoint CEOs under this status regardless of whether they have been elected to the board yet or not;

- Permitting broader delegation of decision-making to “true” executive officers than is currently permitted, but only if independent directors make up a majority of the board of directors. As the Toshiba accounting scandal shows, letting executive-controlled boards delegate more to themselves is not a concept that works very well. At present, “broader delegation” is being vaguely discussed, but clear references to a bright-line condition that would harmonize and strengthen governance (rather than weaken it) are nowhere to be seen. And currently, this condition does not apply in the case of “committee-style” companies.

- Creating mechanisms to ensure that matters for which self-interest invariably affects decision-making – such as director nominations, executive compensation, and related-party transactions such as MBOs or takeovers of subsidiaries – are decided in the independent, objective manner that the corporate governance code requires. This can be done by requiring approval of such items by a “special board” solely made up by independent and disinterested directors (in effect, a binding decision by a “committee”), and shifting the burden of proof when directors are sued by shareholders in cases where such a special board was not used.

- Preventing retired board members (especially, former CEOs and other senior executive officers) from over-influencing decision-making, by requiring disclosure of all aspects of any compensation arrangements such persons have with each company. Such “advisors” are similar to shikkouyakuin in that they have no fiduciary duty or potential liability under the Company Law, yet as senior personages they often participate in decision-making (and inhibit executives) without the consent of shareholders. Their advice may be biased by an obsolete view of competitive dynamics, past internal corporate politics, or the desire to protect their personal “legacy”. At present shareholders have no way of knowing how many such “advisors” exist, what their exact activities are, and what their compensation is – let alone fire them.

At this point, without “political guidance” emanating from the Prime Minister’s office and the LDP, these items are unlikely to be put in place, or even considered much. If this happens, Japan’s corporate governance reform drive will have lost it mojo. There are some things that one can only fix by amending the law, and we cannot expect this particular window to open up again for the next seven years or more.

Nicholas Benes proposed Japan’s Corporate Governance Code and is Representative Director of The Board Director Training Institute of Japan.