Corporate Governance Code Compliance So Far: A Survey of Director Training Policies

The status of director training as required pursuant to Principle 4-14 of the Corporate Governance Code,based on comply/explain disclosures

The Board Director Training Institute of Japan (BDTI)

September 1, 2015

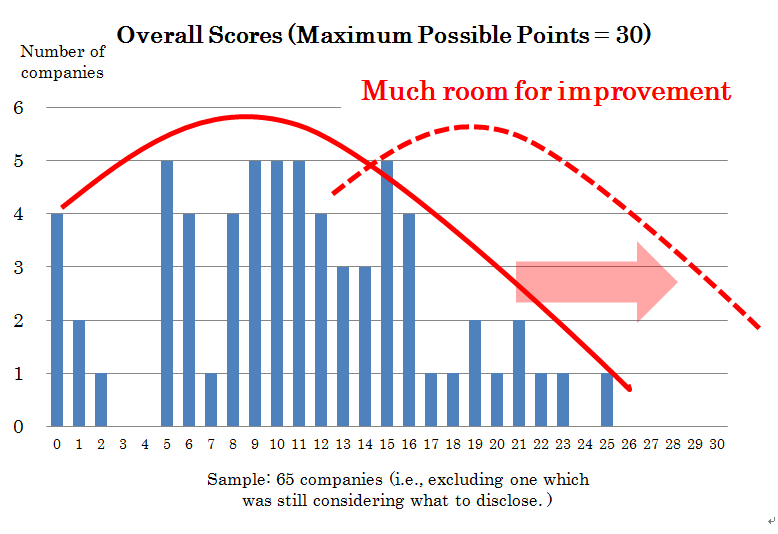

Principle 4.14 of Japan’s Corporate Governance Code (CG Code), requires that companies disclose their policy with regard to the training of directors and statutory auditors. BDTI has analyzed the disclosure about training policy made by the 66 listed companies that filed their corporate governance reports during the period between June 1st and August 7th.

Conclusions

1. The 66 companies should be commended as forerunners, in view of the fact that they have filed their corporate governance reports or disclosed governance guidelines at an early date, and have made a proactive effort to respond to the CG Code. However, overall, in the future we would hope to see greater efforts to “comply or explain”.

2. Many companies make use of the characteristic ambiguity of the Japanese language in order to be vague, and there are many companies that have not really disclosed anything specific about important aspects of their training policies such as the subjects covered, the timing and frequency of the training, or which directors and statutory auditors receive it. When such disclosure is translated into English, the meaning seems even more unclear than in Japanese. Foreign investors may view such content to be insufficient.

3. There is a huge difference in quality of disclosure between the companies which have already commenced director training as their own policy, and those which are commencing director training anew in order to comply with the CG Code, or show no sign of having considered it in depth.

4. Some companies do not seem to understand the full spirit and reasons why a provision about training was included in the CG Code. For example, there are firms that merely provide the outside directors with an “orientation” explaining details about the company, and refer to this as their “training policy for directors and statutory auditors”.

5. We suspect that there may be companies that are not fully disclosing their practices with respect to director training despite the fact that they have concrete, meaningful programs. If disclosure is made but not much is communicated to investors, it is almost meaningless. Such companies need to improve the quality of their disclosure in terms of wording and use of media.

6. Only one company disclosed anything about the actions it actually took with respect to director training in the previous year, notwithstanding the fact that this is the information that investors most wish to know.

7. Some companies have more advanced policies than arguably are required by the CG Code. We expect to see a widening difference in disclosure quality between the leaders and the laggards, with respect to their corporate governance reports and guidelines between leaders.

(Note:20 of the 66 companies also disclosed English versions of their corporate governance reports.)

Scores of the Top Rated Companies (maximum obtainable score: 30 points)

Points

Company

25

Daito Trust Construction

23

Jtekt

22

Shiseido

21

Kawasaki Heavy Industries, Eisai

20

Toyota Boshoku

19

Omron, Honda Tsushin Kogyo

Reference: Japan’s Corporate Governance Code Principle 4.14

Principle 4.14 Director andKansayakuTraining

New and incumbent directors andkansayakushould deepen their understanding of their roles and responsibilities as a critical governance body at a company, and should endeavor to acquire and update necessary knowledge and skills. Accordingly, companies should provide and arrange training opportunities suitable to each director andkansayakualong with financial support for associated expenses. The board should verify whether such opportunities and support are appropriately provided.

Supplementary Principles

4-14-1 Directors and kansayaku, including outside directors and outside kansayaku, should be given the opportunity when assuming their position to acquire necessary knowledge on the company’s business, finances, organization and other matters, and fully understand the roles and responsibilities, including legal liabilities, expected of them. Incumbent directors should also be given a continuing opportunity to renew and update such knowledge as necessary.

4-14-2 Companies should disclose their training policy for directors andkansayaku.

Summary of Analysis

Survey Universe

The 66 listed companies filing their corporate governance reports during the periods, between June 1stand August 7th, 2015

Date

August, 2015

Methodology

We rated the each company’s disclosure about its implementation of Principle 4.14 as set forth in their corporate governance reports or guidelines (or other materials referred to in such reports). We analyzed 11 factors (aspects) which were weighted for their relative significance, and calculated the overall score for each company, based on a maximum obtainable score of 30 points.

DDisclaimer

The evaluations in the report described by this release are based on review of the corporate governance reports submitted by each firm, and other disclosed materials referred to therein. The evaluations are not, and do not purport to be, comprehensive analyses of the actual status of director training at each company.

In order to ensure objectivity and fairness, the evaluations described in this release are based on scoring criteria developed by BDTI. However, even then, subjective judgments must be made with respect to the nuances of wording in disclosed materials, or the overall impression created by disclosures.

This release does not constitute advice for the purposes of making investment decisions or decisions about investment policy. In no case in which the reading of this release is asserted to have caused damage of any type shall BDTI shall bear liability or responsibility with regard to such damage.