“….As announced in our policy guidelines last year, beginning in 2019, for companies listed on the first and second sections of the TSE, we will begin making recommendations against members of a board that does not have any incumbent or proposed female members. In such instances, we will generally recommend voting against the chair of the company (or the most senior executive in the absence of a company chair) under the two-tier board or one-tier with one committee structures, or against the nominating committee chair under a one-tier with three committees structure. In the case of a two-tier board structure, we will examine the board of directors and board of statutory auditors as a whole, and in the cases of one-tier with three- committee structures, we will consider whether the company has any female executive officers as well as female directors.

Category: ESG

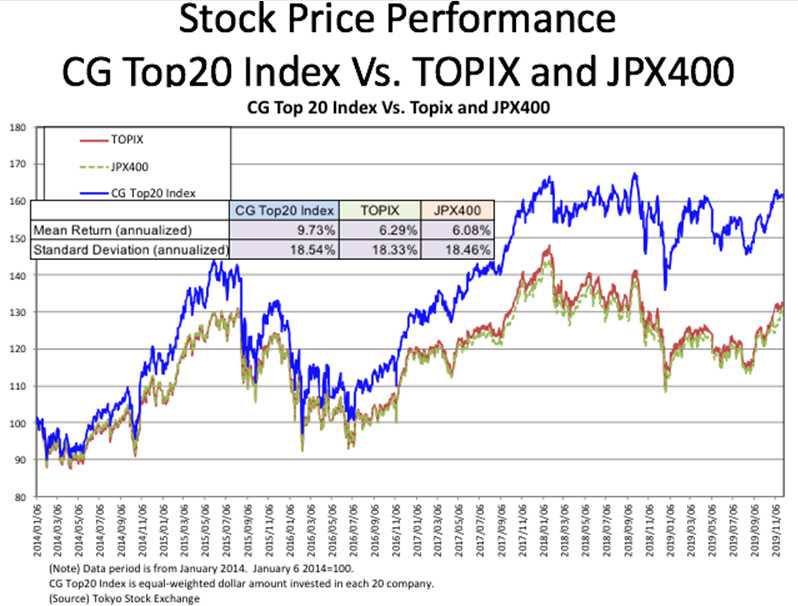

Metrical:”November Market Indices and CG Top 20 stocks kept higher.”

Stock prices closed higher amid risk-on mood from the previous month. TOPIX and JPX400 market indices gained 0.10% and 0.08% respectively for the month. CG Top 20 stocks rose modestly by 0.04% for the same period.

Metrical:”Ex-CEO advisors”

This month METRICAL shows how the disclosure about ex-CEO advisors has progressed from a year ago. As shown the table below, in October 2018, 829 companies on METRICAL’s research universe disclosed the number of ex-CEOs (ex- Representative Directors) who retained positions as “advisor” in the company after stepping down as CEO. Of these companies that voluntarily disclosed, 474 companies had ex-CEO advisors. A year later in October 2019, a total of 894 companies disclosed the number of ex-CEOs who retained such advisory positions seat in the company after stepping down from the top management position. Of these 894 companies, 503 companies had ex-CEO advisors in October 2019.

“Japan’s Unfinished Corporate Governance Reforms”, by Nicholas Benes

My article on Japan’s unfinished reforms is online now. Lest the Abe administration and regulators “declare victory” when they are only half done, I describe seven specific measures that Japan needs to adopt in order to bring its market up to a global standard for a developed nation:

- Detailed rules for an independent committee

- A clear requirement for a majority of independent directors on the board

- Codifying the role and responsibilities of executive officers

- Consolidation of overlapping disclosure reports

- Protection of minority shareholder rights

- Enhancing transparency to reduce entrenchment and enhance inclusiveness

- Strengthening stewardship throughout the investment chain

I stress the reality that in all of these, strong political leadership from the Prime Minister and other senior parliamentarians will be needed. “Thus, is it essential that the Tokyo Stock Exchange (JPX/TSE) and the various regulatory agencies keep up reform momentum. However, one senses a desire from these groups to ‘declare victory’, and they have a tendency to not fully coordinate with each other. If Prime Minister Abe’s cabinet did more to make the key players coordinate their efforts in key areas, meaningful governance change (and protection of investors) would accelerate….

Japan Times “Compelling Need for Adoption of ESG Goals”

“Intensifying pressure to limit global temperature increases and prevent ecological disaster is mounting and corporations and investors — including those in Japan — have an urgent role to play.

That was a key message at the CDP Forum on Decarbonizing Management — Vision to Action held in Tokyo on Nov. 19.

Investing.com:“Japan is the Place to Invest” By Cumberland Advisors

“ ….The OECD notes that, despite the current slowdown, the expansion of the Japanese economy that began in late 2012 is the longest in Japan’s postwar history and is projected to continue through 2020. The Bank of Japan’s forecast is similar, with a pick-up in growth expected in Japan’s fiscal year 2021. Continued supportive monetary policy with very low interest rates and large-scale government bond purchases, together with increased public investment and spending to offset the effects of the sales-tax increase, are expected to maintain the expansion. The new U.S.-Japan trade deal and the anticipated elimination of the threat of U.S. automobile tariffs are positive developments. If the current optimism about progress in trade talks between the U.S. and China proves to be justified, Japan’s economy would benefit significantly from the positive effects on the Asia region….“

TIIP:”Sustainable Investing in Japan: An Agenda for Action”

Executive Summary

More than a quarter of assets under management (AUM) worldwide are invested in “sustainable” strategies, strategies that consider environmental, social, and governance (ESG) factors in pursuit of financial sustainability and/or environmental or social sustainability. Investors – both individual and institutional and at all wealth levels – are increasingly interested in integrating these strategies into their financial plans and investment portfolios, and asset managers and global financial institutions are embracing the approach and expanding related services and product offerings.

Interest in sustainable investing and sustainably invested AUM are growing rapidly in Japan. But despite this enthusiasm and growth, few mainstream investors, financial advisors, and investment consultants in Japan are embracing the practice.

METRICAL/BDTI:Ratings of 1,800 companies (July 2019 Update)

In our July ratings, a more nuanced pictured emerged for Japanese companies. The significantly positive correlation of financial performance with the percentage of INEDs and the number of Female Directors disappeared this month, suggesting that an increasing number of non-superior performers are “copying” other companies in this respect, and/or have only only done so recently so no positive impact (should there be any) is discernible.

Disclosure of Executive Compensation Required by New Cabinet Office Order… and Companies’ Responses

On January 31, 2019, the Cabinet Office Order on Disclosure of Corporate Affairs was amended, and the format of for securities reports was changed. With regard to the securities reports for the fiscal year ending March 2019, it is said that the employees in charge of dealing with the new format were put under considerable stress and extra work. The most troubling item was probably the section on executive compensation.

The revision of the Cabinet Office Order was made in response to the Financial Council Disclosure Working Group (DWG) report published on June 28, 2018. Mr. Carlos Ghosn was arrested in November of the same year, and executive compensation, which has been a subject of much debate for some time, once again disturbed the public mind. The new format, modified under these circumstances, calls for broader and detailed information disclosure. However, the top executives of many companies view disclosure of compensation as undesirable, because it has carries the potential for divisiveness or embarrassment. Mr. Ghosn’s false statement of compensation was attributable to this sense of aversion. Not only him, but also many other executives, desire as a basic human emotion to avoid disclosure of the amount of their compensation.

What were these two contradictory vectors, – requirements from Cabinet Office Order, and the company leaders’ intentions – reflected securities reports? Although we should wait for the thorough analysis on many securities reports published at the end of June 2019, in this article I would like to convey the initial impression that I obtained by surveying a few of them.

Japanese Institutional Investors Need to Take Their Own ESG Medicine

Does anyone have any theories as to why institutional investors that support director training in Japan are overwhelmingly foreign, and not Japanese?

The Board Director Training Institute of Japan (BDTI) was established as a “public interest” nonprofit in order to enable Japanese institutional investors to support something badly needed by their home market, director and governance training, on a tax-deductible basis…. so that such training could be offered at high quality yet low price, thereby spreading customs of governance/director training throughout Japan. However, after running BDTI for eight years since obtaining certification, we have noticed a disturbing but continuing reality: over time, more than 95% of BDTI’s donations from institutional investors have come from foreign institutions or fund managers, and less than 5% of donations to BDTI have come from Japanese institutions. Moreover, none of the Japanese institutional donors are “major” (top 30) investing institutions in Japan.